VUCA. VUCA. VUCA.

This is not how I would normally start an article but it’s an acronym I’m guilty of over-using lately. I honestly just learned of it only last year from a mentor at a scholarship program I was enrolled in. If this is the first time you’ve heard of VUCA then I guess you can thank me because you’re going to hear a lot more of VUCA for the time to come. Trust me. VUCA stands for Volatility — Uncertainty — Complexity — Ambiguity. The acronym was first used in 1987 to describe circumstances at the end of the cold war. Let me put VUCA into context for you: a global economic crisis is looming on the horizon; powerhouse economies on the brink of collapse. Don’t believe me? Bloomberg economists Eliza Winger, Shulyatyeva, Andrew Husby and Carl Riccadonna developed a model using indicators like unemployment and stock prices to determine the odds of recession. And the result…..

A staggering 100%! Inevitable recession in the next 12 months! But what’s all this fuss about? I mean we’ve seen financial crises before — least once every decade. Well only this time it’s much worse. To support this, senior economist Nouriel Roubini likened the current and upcoming crisis to no other. “So, this is just something we’ve not really seen before. It is a bit like as if an asteroid hit the Earth”. During the global financial crisis of 2008, there was a two-year buffer from the unraveling of the US housing market and mortgages before the eventual collapse of Lehman. Furthermore, it also took two years for the stock market to fall 30% in that same crisis. This time around, it only took less than a month before economic activity collapsed and the stock market took a toll. With the world going into economic freefall, it’s no surprise that we are going to see a lot of defaults in the global debt market and anyone tied to the system will surely bear the repercussions. Yikes! That’s crazy talk!

You see, on a macro level, traditionally the banking sector stimulates economic growth/economic recovery through borrowing schemes. Economic growth is supported by adequate levels of capital circulating in the economy. That, in turn, will make-way for ideal business conditions as credit expansions will increase investments and consumption. An increased economic activity means more jobs and more profit for the company; this means prosperity for the country. With an exhausted banking sector, we’ll begin to wonder who is going to fill that void and stimulate economic growth/recovery. We’ll also begin to wonder if there is a model that works just as well, if not, better than the capitalism model.

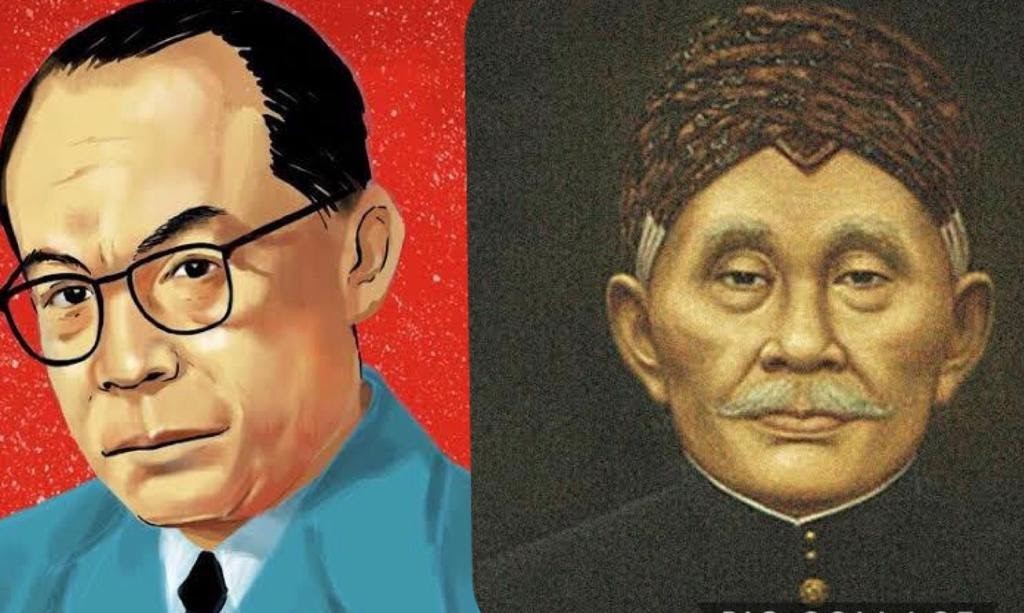

I often wonder if Gen Y-Z is still familiar with the concept of koperasi. The same koperasi concept Bung Hatta is famously known for: a vehicle for civil economy. The man is widely known as the ‘Father of Koperasi’ here in Indonesia. That’s a pretty big deal! Or if we go further back to 1896, you would probably have heard of Patih Raden Arya Wiryaatmaja. I mean who hasn’t right? He was the famous Regent of Purwokerto. Wanna know why else he was famous? Ever heard the story of ‘Hulp-en Spaar’ or ‘Bank of the People’. Yeah, Patih Raden Arya Wiryaatmaja founded the Hulp-en Spaar to save his people from falling into the trap of loan sharks. Oh, and btw, that ‘Bank of the People’ is known as ‘Bank Rakyat Indonesia’ today. The biggest state-owned bank as it stands.

Did you know that Indonesia boasts 150,000+ koperasi and 28 million +(2019) koperasi members? That’s more than any other country in the world! The majority of Indonesian koperasis are Koperasi Simpan Pinjam or KSP. KSP translates to savings and loans. KSP are traditional institutions that lend money to its members. KSP operates very much like traditional banking models. Both institution and models involve collecting funds from members and then allocating those funds back to members as borrowings. The only major difference is that banks are profit-driven whilst koperasis operate to increase the welfare of its members. Well you would argue that both are for profit and ultimately increases the wealth of those who own shares in them. But here’s how a koperasi system works differently: koperasis are a traditional equity-crowdfunding platform that is communally owned and democratically governed by those who use the products and services their business produces. In other words, its members.

As Indonesians, koperasi is ingrained in our DNA. You’ll also find that there is an uncanny resemblance/underlying theme in the 7 koperasi principles and the 5 principles in which Indonesia was founded on (Pancasila). Sadly, I often don’t get the affirmative answer to my koperasi inquiries — especially with the youths. You can try inquiring and vindicate my article later. For the older generation, koperasi is something profound — something of inheritance value. That’s really all it comes down to right now. But let’s not downplay their significance just yet. Koperasis and SME’s account for 65% of Indonesian GDP annually. Historical data has also shown that koperasis and SMEs have proven to be more resilient towards economic crises. In the 1998 monetary crisis, SMEs fared much better in comparison to it’s larger corporate counterparts. SMEs and koperasis were able to survive the crisis because the majority of them were not dependent on high capitalization and loans in foreign currencies. It is also worth noting that SMEs and koperasis are responsible for providing jobs to almost half of the Indonesian population (depkop.go.id). So we’ve established that koperasis and SMEs should be a priority in building a strong backbone for the Indonesian economy. There is usually a thin line between koperasis and SMEs because they are either an umbrella of one another or they operate in parallel with each other. Koperasis and SMEs have always been a synergy, hence why they have a joint Ministry dedicated to them.

Only recently, the Indonesian government has emphasized on digitizing this highly underserved space. Do you know what that means? By disrupting the traditional koperasi model and making it accessible and accountable, the government is enabling koperasis to serve beyond Indonesia’s 65% underbanked population and make way for greater financial access and inclusion – to further democratize financial services. Koperasis have long been instrumental in driving financial inclusion here in Indonesia. That’s right, even before things were difficult for the banking sector. Koperasis have excelled where banks have struggled. Banks have an untold history of scrambling in formulating an effective distribution model to serve Indonesia’s underbanked population across > 17,5000 islands. Whilst banks were scratching their heads over adoption dilemmas, koperasis have always been around as your friendly neighborhood superhero when it came to community-based economics.

Better infrastructure has led to a recent 4.6% surge (15 million people) in mobile connectivity nationwide. That’s a 338.2 million mobile connections recorded as of January 2020.

To put that into context: 124% of the country is connected! That’s insane! In addition to this, recent study also recorded a 25% surge in nationwide internet users and 59% of all Indonesians are now on social media — making it a powerful communication tool. So far, the majority of koperasis have been reduced to excel in managing finances and Facebook to engage existing as well as potential members. This may have a lot to do with demographics of its members; predominantly people in older age groups. However, if koperasis are able to leverage on the recent insurgence of technological advancements and adopt it, then they would be able to sustainably scale. Joining in the bandwagon with technological advancements will help koperasis streamline current processes to achieve organizational efficiency. At the same time, social technologies will enable these koperasis to reach a wider audience. If koperasis are able to play their cards right, they will have a bigger piece of the pie than they have ever had before.

Koperasis traditionally operate at a micro level and that is why they are the people’s champion. Because of their community-centric nature and the close-knit relationship of their ecosystem, koperasis are still able to operate traditionally and tend to those other financial institutions would have trouble in credit scoring. Although you may deem them as rookies for the part they play in the economy, but given the volume at which they operate in Indonesia, and with the right catalyst to effectively scale, collectively, we’re looking at dark knight(s) who have been operating in their own silo towards the revival of the Indonesian economy.

Article Link:

https://medium.com/vis-indonesia/a-brave-new-world-4eab08a47717